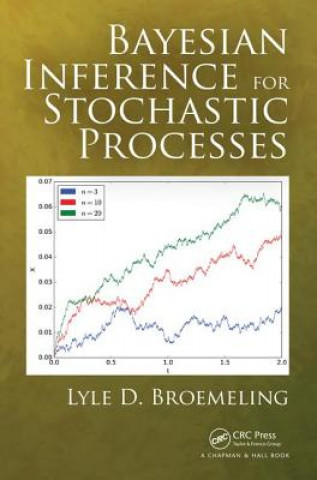

Bayesian Inference for Stochastic Processes

Autor:

Lyle D. Broemeling

Dostupnost:

50 % šance

Prohledáme celý svět

5 283

Kč

This is the first book designed to introduce Bayesian inference procedures for stochastic processes....